Macrs Life Of Solar Panels

Macrs For Commercial Solar Panel Installation

Guide To The Macrs Depreciation Method Chamber Of Commerce

Macrs Green Energy Home Office Incentives Go Solar Group

Heatspring Magazine Finance 101 For Solar Pv Professionals

An Introduction To Solar Depreciation Yellowlite

Battery Storage Systems Federal Tax Incentives Nrel

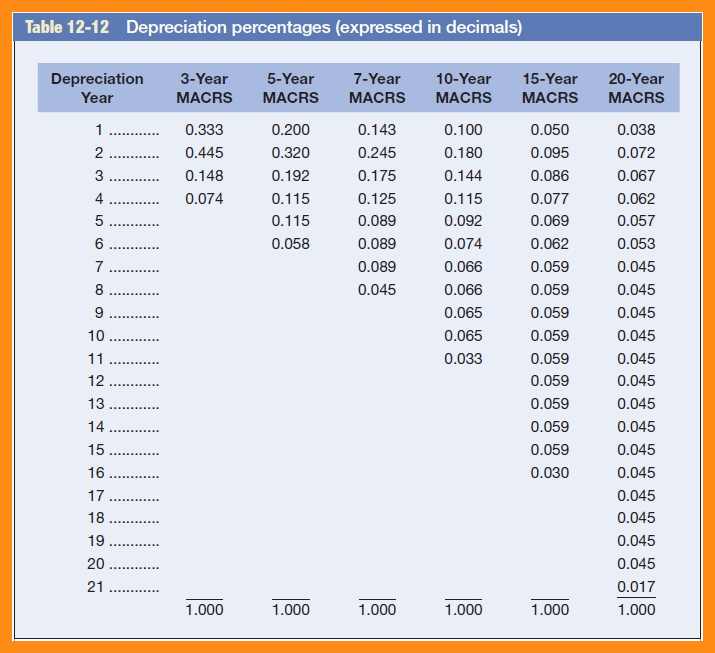

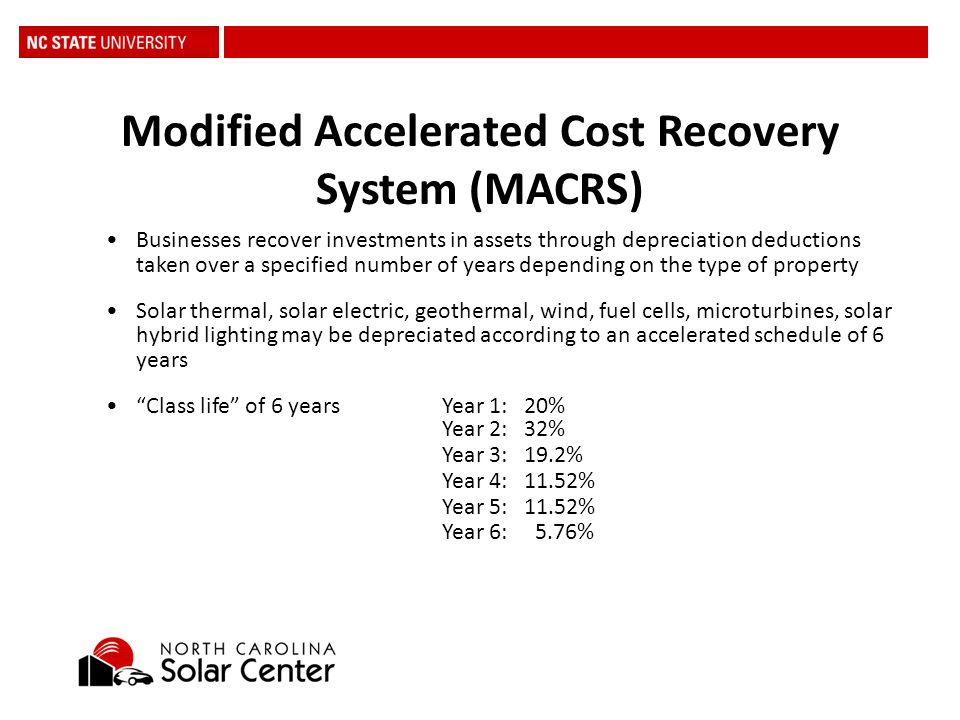

Commercial solar power systems are eligible to be depreciated over a 5 year accelerated rate schedule.

Macrs life of solar panels.

What Is The Modified Accelerated Cost Recovery System Macrs

Primer On Bonus Depreciation Scottmadden

Sunedison Inc Responds To Claims And Allegations Made By Terraform Power Inc And Terraform Global Inc Solar News Global Power

2020 Guide To Solar Tax Credit Rebates And Other Incentives

Solar 101 Sunvalley Solar

Renewable Energy Tax Incentives

Macrs Depreciation For Solar One Major Tax Benefit Of Installing Solar Energylink

Commercial Depreciation On A Solar Energy System Yellowlite

Solar Tax Credits And Benefits Part 2 Of Our Commercial Solar Installation

Accelerated Depreciation Can Accelerate Your Business Going Solar

Ipsun Power Explaining Solar At Public Event Solar Solar House Power

4562 Half Year Mid Month And Mid Quarter Conventions 1120 1120s 4562

Solar Panel Costs Solar Consultant

Yield Based Flip And Partnership Allocation Generally For Wind Projects Edward Bodmer Project And Corporate Finance

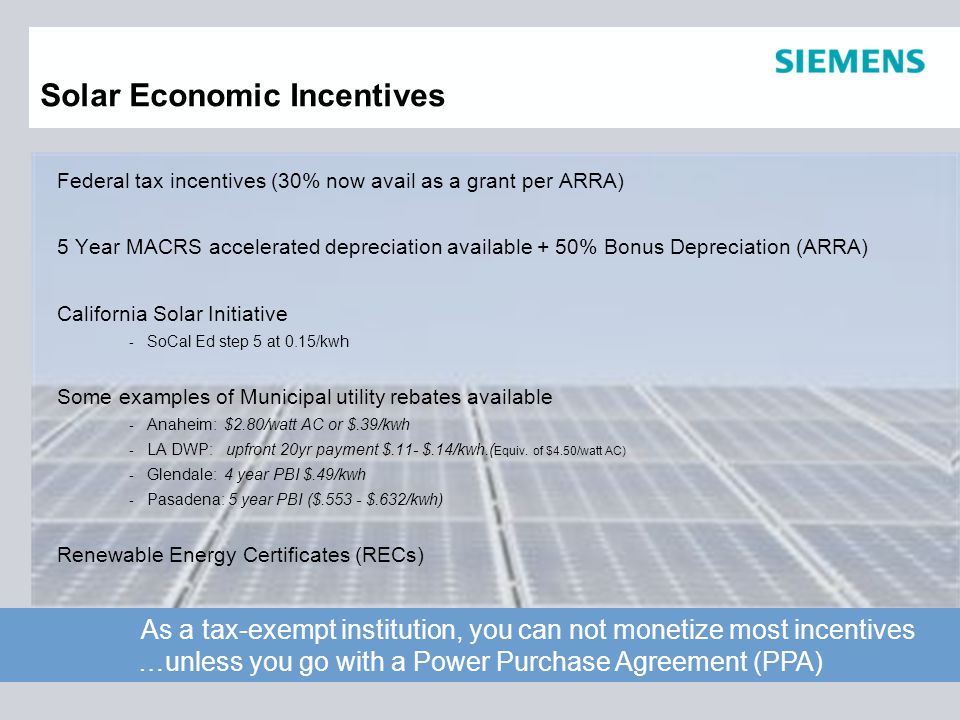

Siemens Building Technologies Renewable Energy Laura Berland Shane Siemens Building Technologies Ocbc Presentation July 14 Ppt Download

Us Levelized Cost Of Energy By Technology H Mwh Ppt Download

Public Policy Economics Ppt Video Online Download

Southern Light Solarmassachusetts Commercial Federal Solar Tax Credits Southern Light Solar

Solar Energy Costs For Mc Gehee Kelsey

Solar Sign Products Solar Sign Kits Solartech Sign

Solar Tax Benefits Remain Powerful 2019 Recap Revision Energy

Sharon Canavan Office Of The Comptroller Of The Currency Stephen Tracy Ppt Download

Solar Energy For Business A Complete Guide Rec Solar

.jpg)

Interpv Net Global Photovoltaic Business Magazine

Source : pinterest.com